Monthly Market Review: Markets rally as attention shifts to inflation, rates

Markets rallied strongly in April, with the global benchmark for stocks rising 7.2% and several regional markets hitting all-time highs.

Although the Strait of Hormuz remained close through most of the month, the end of the bombing campaign by the US and Israel appeared to assuage market concerns and increased belief that a negotiated outcome could be reached. Attention has shifted to the path for inflation and interest rates, with the economy so far absorbing much of the price shock.

Iran War and Energy Markets

The ongoing conflict in the Middle East remained the key driver of market direction. Brent oil hit the highest since 2022 during the month, with refined products, particularly diesel and jet fuel, experiencing significant supply constraints. These disruptions are increasingly feeding into global supply chains, raising concerns about broader economic impacts.

Inflation and Central Bank Outlook

Monetary policy expectations shifted over the month, with previous optimism around rate cuts fading. Although most Central Banks have held rates steady at recent meetings voting patterns have indicated a more cautious stance in response to energy-driven inflation, reinforcing a “higher-for-longer” rate environment.

Economic Data and Growth Trends

Economic data released during the month was generally robust, with business confidence indictors holding up and employment showing improvement. Contrasting this is the growing hit from higher energy prices which is feeding through to consumers and has knocked back confidence levels.

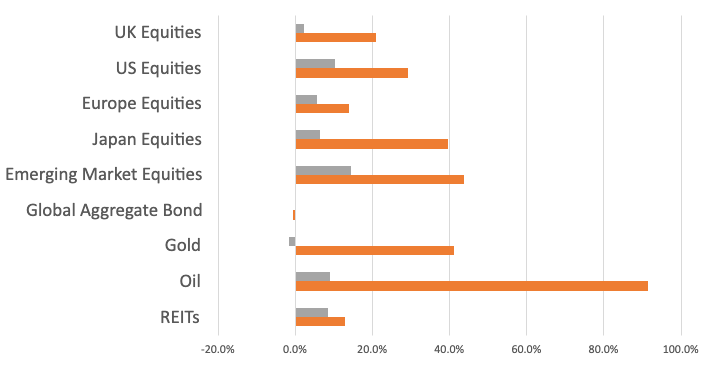

Asset Class Summary

Past performance is not a reliable indicator of current or future returns.

Data source: Fundment

Emerging Market Equities: +14.5% and top performer in April, after being the weakest performer in March, with economic risks reduced

UK Equities: +2.4%, weakest performing market in April amid lacklustre economic performance, with the IMF downgrading UK growth more than any other major economy

US Equities: +10.4%, second best performer with tech stocks continuing to outperform

Energy: Brent oil +9.1% in March and 91.6% YoY

Gold: -1.5%, reduced geopolitical risks allowed for a small decline after strong run

Bonds: Yields rose further amid higher for longer inflation expectations

Areas to watch

Middle East Conflict: The outcome of negotiations and ongoing blockade of the Straits of Hormuz will remain central to market direction

Inflation: The impact of supply constraints is increasingly showing up in inflation data, with the debate centred on the likely stickiness of price increases.

Monetary Policy: The debate has shifted away from the potential of cuts to hikes, with rate setters sounding increasingly hawkish

News

UK

GDP grew by 0.6% in the first quarter, the best reading in a year as the economy appeared to hold up in the initial period of the Iran war.

UK unemployment unexpectedly rose to 5% while job vacancies fell to a five-year low, amid early signs the Iran war is starting to weigh on business confidence.

The UK Composite PMI picked up to 52.0 in April from 50.3 previously with both services and manufacturers seeing an upswing, although some caution appears warranted as revenue was boosted by a large increase in inventory levels.

US

Producer Price Inflation jumped to 6% in April, from 4.3% previous, as the impact of higher energy prices began to feed through.

Retail Sales jumped by 1.7% MoM in March, the fastest pace in 3 years and boosted by higher gasoline spending, but with other areas also holding up well.

The ISM Manufacturing confidence indicator held steady at a respectable 52.7 despite an input price surge.

China

Exports rebounded faster than expected in April, rising 14.1% YoY ahead of 2.5% growth in March, while Import growth also accelerated to 25.3% YoY.

Industrial Output disappointed at 4.1% YoY growth in April, the weakest in 3 years, while Retail Sales (0.2% YoY) and Fixed Asset Investment (-1.6% YoY) also disappointed in a weak set of monthly data.

The Official Composite PMI dropped back to 50.1 from 50.5 with a breakdown of the data indicating a mixed picture with domestic demand continuing to weaken while export demand remains firm.

Europe

CPI Inflation rose further to 3.0% YoY in April, from 2.6% in March, however the Core reading excluding energy prices remained stable at 2.2%.

The trade deficit with China surged to $83bn in the first quarter, with imported electric vehicle sales more than doubling as China’s exporters made headways into EU markets after increased barriers to trade with the US.

The Eurozone Composite PMI confidence dropped to a 17-month low of 48.6, from 50.7 previously, with inflationary pressures and supply outages pressuring demand.

Others

Taiwan Q1 GDP smashed all expectations, rising 13.7% YoY as semiconductor exports surged in response to the AI boom, with the country responsible for around 90% of advanced AI chip production.

The UAE, in an apparently unexpected move, announced plans to leave the OPEC+ group in a bid to boost production levels, a move that is likely to pressure the Cartel’s influence and potentially reduce oil prices.

Important Information

This communication is intended for financial advisers and other investment professionals only.

Past performance (including simulated or back-tested data) is not a reliable indicator of future results.

Investment values can go down as well as up, and clients may get back less than they invest.

Fundment does not provide investment advice or recommendations. Investment selection remains entirely at advisers’ discretion.